Shell India Markets Pvt. Ltd. vs DCIT: ITAT Mumbai Sets Aside ₹536.76 Crores in Transfer Pricing Adjustments

Comprehensive analysis of landmark ruling establishing critical precedent on contemporaneous data requirements, functional comparability, and Production Sharing Contract frameworks

The ITAT Mumbai’s decision in Shell India Markets Private Limited addresses fundamental procedural requirements under India’s transfer pricing regulations while recognizing the commercial reality of complex, industry-specific operational frameworks. The ruling provides critical guidance on five key areas that will shape transfer pricing compliance and dispute resolution for years to come.

Company Profile and Business Operations

Shell India Markets Private Limited operates as the Indian subsidiary of Royal Dutch Shell Group, engaged in comprehensive downstream oil and gas operations across multiple business verticals. The company’s operations for Assessment Year 2020-21 encompassed:

- Petroleum retail distribution network management

- Lubricants manufacturing and supply chain operations

- Bitumen trading and distribution

- Liquified Natural Gas (LNG) terminal operations

- Specialized technology services for group entities

- Upstream exploration and production (E&P) technical support services

- Centralized shared financial services and back-office support

For the relevant assessment year, Shell India Markets filed returns declaring total income of INR 215.80 crores after voluntarily applying a 12% transfer pricing markup on intra-group services provided to associated enterprises, demonstrating proactive compliance intent.

Overview of Transfer Pricing Adjustments Challenged

The Transfer Pricing Officer (TPO) and Dispute Resolution Panel (DRP) imposed aggregate transfer pricing adjustments of INR 536.76 crores across five distinct business segments. Each adjustment presented unique methodological challenges and substantive issues:

| Business Segment | Adjustment Amount (INR Crores) | TP Method Applied | Primary Issue Identified |

|---|---|---|---|

| SBO IT Services – Bengaluru Operations | 109.94 | TNMM | Use of non-contemporaneous comparables from AY 2017-18; application of arbitrary turnover filters without economic justification |

| SBO Services – Chennai Operations | 102.57 | TNMM | Reliance on stale prior-year comparables; inclusion of large brand-intensive entities (Infosys BPM, Tech Mahindra) despite fundamental functional differences |

| Exploration & Production Technical Services | 48.63 | TNMM (inappropriate application) | Rejection of at-cost recovery model mandated by Production Sharing Contract (PSC) regulatory framework; complete disregard of PSC legal requirements |

| Group Cost Allocation Charges | 269.01 | “Other Method” (undefined) | Determination of nil arm’s length price without proper benchmarking analysis or reference to comparable transactions as required under Section 92C |

| Salary Cost Recoveries | 6.61 | TNMM | Recharacterization of genuine pass-through cost recoveries as fee-based service transactions requiring profit markup |

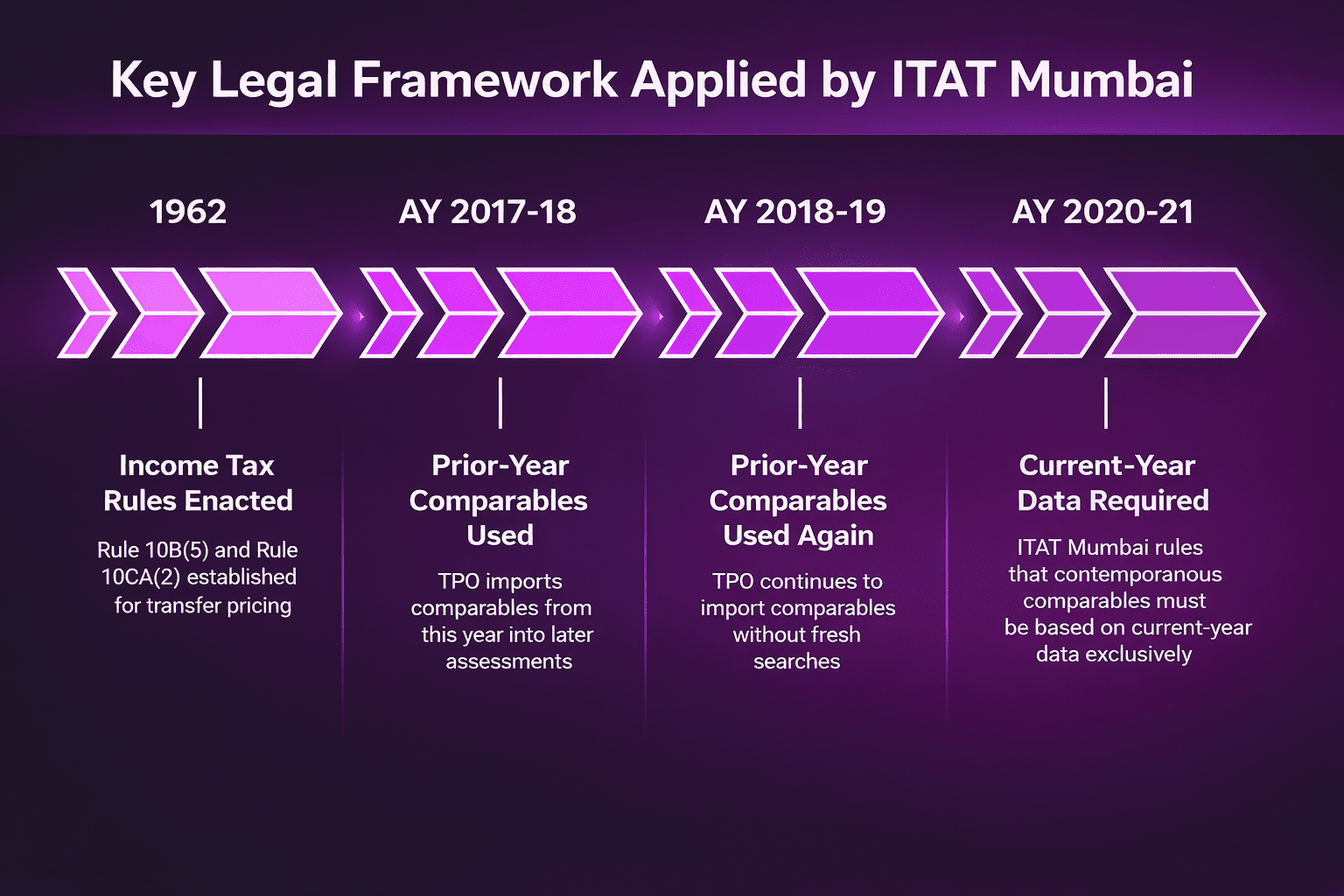

Legal Framework: Contemporaneous Data Requirement Under Rule 10B(5)

Figure 1: Evolution of contemporaneous comparable data requirements – from Rule 10B(5) statutory enactment through systematic prior-year comparable reuse to ITAT Mumbai’s definitive ruling requiring exclusively current-year data

The tribunal applied Rule 10B(5) read with Rule 10CA(2) of the Income Tax Rules, 1962, establishing the fundamental statutory principle that contemporaneous comparables for transfer pricing analysis must be based exclusively on current-year financial data. The use of prior-year comparables is permitted only as a narrow exception when current-year data is genuinely unavailable at the time of return filing—a circumstance that cannot be manufactured through administrative convenience or resource constraints.

Critical Holding: Contemporaneous Data Mandate

The tribunal determined that the Transfer Pricing Officer fundamentally failed its statutory duty by mechanically importing comparable company selections from assessments completed for AY 2017-18 and 2018-19 into the AY 2020-21 assessment without conducting any fresh search for contemporaneous comparable data. This practice violates the express statutory scheme embodied in Rule 10B(5) and systematically undermines the reliability and accuracy of transfer pricing determinations.

This ruling definitively closes a procedural loophole that had enabled revenue authorities to recycle outdated comparable company datasets across multiple assessment years, creating systemic distortion in transfer pricing outcomes while simultaneously imposing unjustified compliance burdens on taxpayers who had properly selected current-year comparable data in accordance with statutory requirements.

Detailed Tribunal Findings and Binding Directions

Issue I: SBO IT Services Bengaluru Segment – Remanded for Fresh Assessment

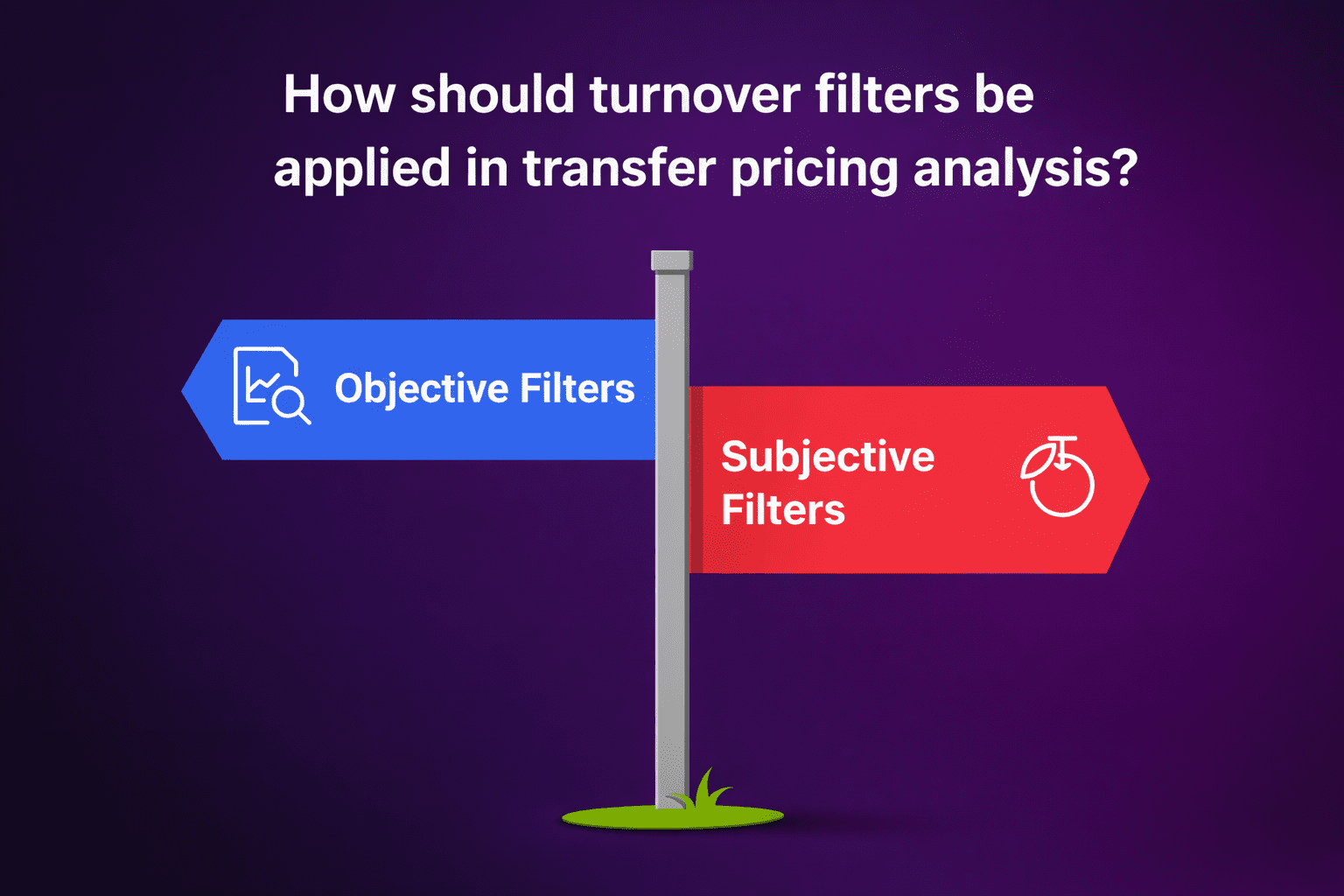

The tribunal identified fundamental procedural violations in the Transfer Pricing Officer’s approach to this segment. The TPO applied comparable company selections identified three years prior for AY 2017-18 without any fresh contemporaneous search for the relevant AY 2020-21 assessment period. More critically, the introduction of arbitrary turnover filters—specifically the mechanistic application of 1/10 to 10 times revenue band without economic justification—constituted impermissible “cherry-picking” designed to exclude functionally comparable entities that would otherwise support the assessee’s transfer pricing position.

Figure 2: Critical distinction between permissible objective filters (minimum revenue thresholds to ensure data quality by excluding defunct or startup entities) versus prohibited subjective filters (arbitrary mechanical turnover bands lacking economic logic or empirical validation)

Landmark Principle: Prohibition on Post-Hoc Filter Application

The tribunal held that turnover-based or size-based filters cannot be deployed as post-hoc exclusion tools to eliminate comparables already determined to be functionally equivalent through detailed functional, asset, and risk (FAR) analysis. The bench drew a critical distinction between objective filters designed to ensure data quality and reliability versus subjective mechanical bands that lack inherent economic logic or empirical validation in the specific industry context.

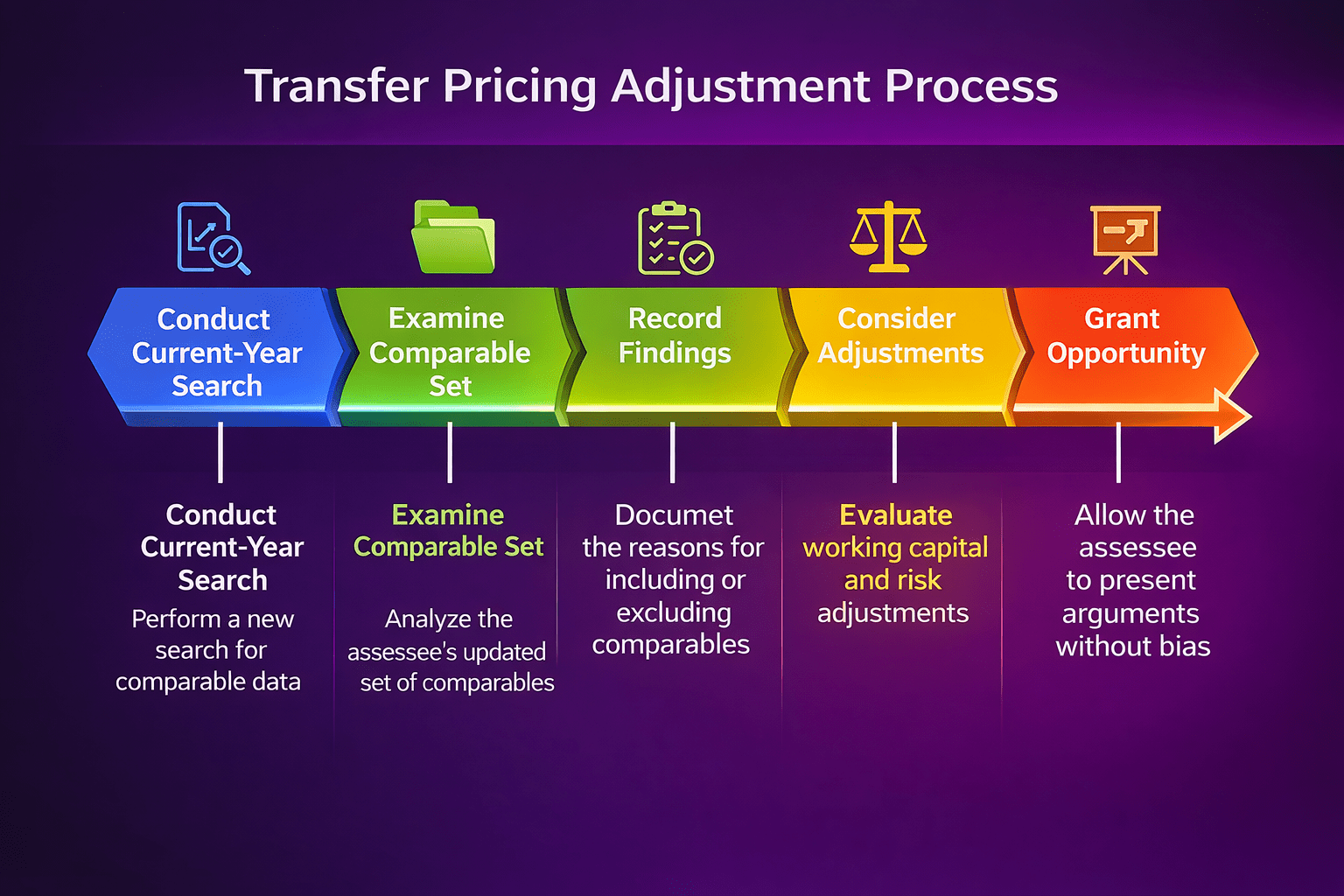

Figure 3: Comprehensive five-step procedural framework mandated by the tribunal for proper transfer pricing assessment and determination of arm’s length adjustments

Binding Directions to Lower Authorities

- Fresh Contemporaneous Search: Conduct entirely new comparable company search using exclusively current-year (AY 2020-21) financial data in strict accordance with Rule 10B(5) statutory requirements

- Detailed FAR Analysis: Examine the assessee’s freshly proposed comparable company set with comprehensive qualitative analysis of functional profile, asset deployment, and risk assumption characteristics

- Reasoned Findings: Record detailed, specific economic rationale for inclusion or exclusion of each proposed comparable entity, supported by explicit reference to functional differences or similarities

- Substantive Adjustment Consideration: Evaluate working capital adjustments and risk profile adjustments on their merits rather than dismissing them summarily without analysis

- Fair Hearing: Provide genuine opportunity for the assessee to present comprehensive arguments without being influenced by the earlier erroneous rejection

Issue II: SBO Services Chennai Segment – Remanded for Fresh Assessment

Similar to the Bengaluru segment, the tribunal found that the Transfer Pricing Officer relied on prior-year comparables (specifically Infosys BPM and Tech Mahindra Business Services) without conducting any contemporaneous analysis for the relevant assessment year. These comparables represent large, brand-intensive business process management entities that are fundamentally incomparable to a captive, low-risk shared services center providing routine back-office functions under controlled conditions.

The tribunal directed comprehensive de novo functional, asset, and risk-based current-year analysis, specifically requiring examination of the assessee’s eight proposed comparables with comprehensive recorded reasons for acceptance or rejection of each entity.

Issue III: Exploration & Production Technical Services – Adjustment Entirely Deleted

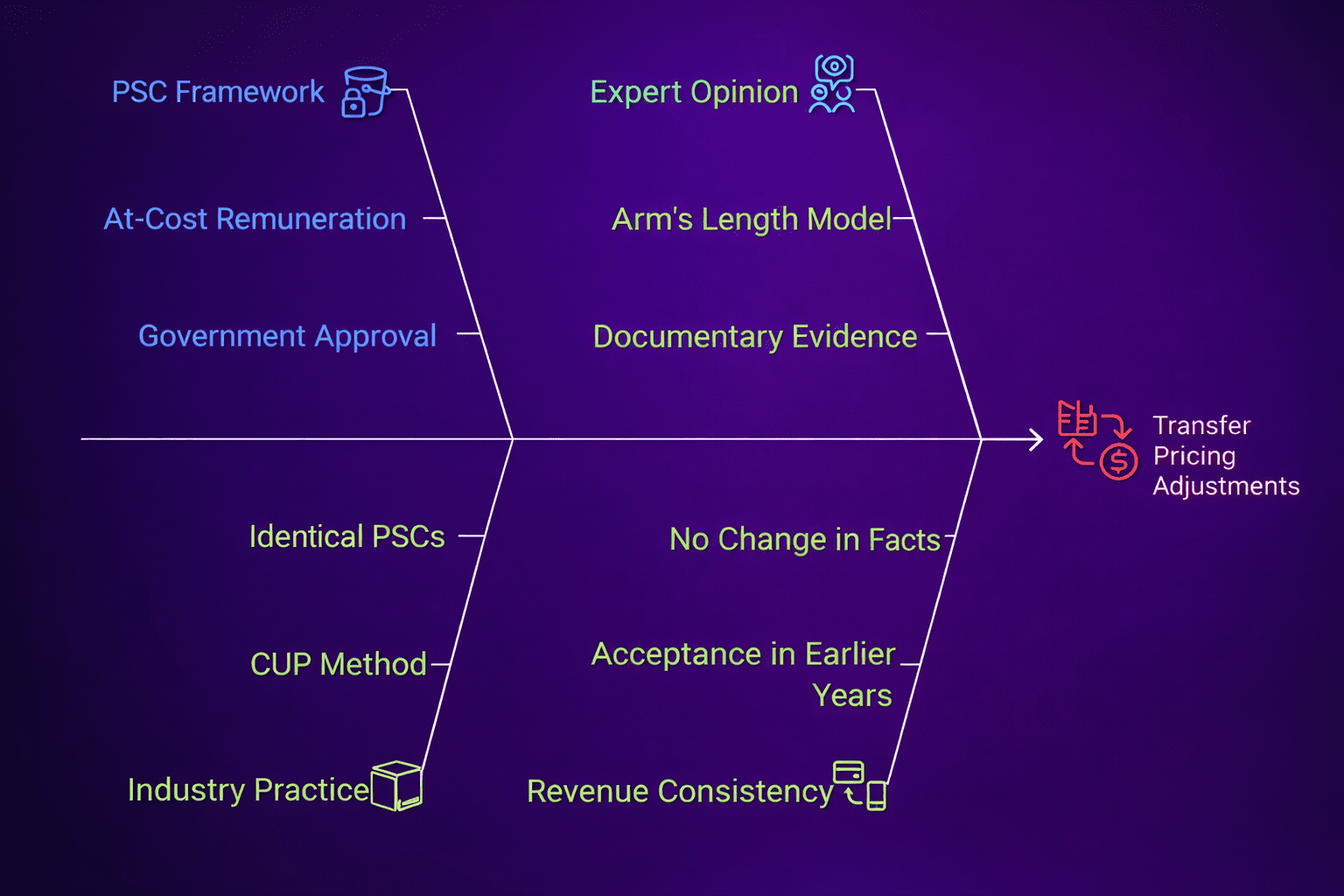

The tribunal entirely deleted the INR 48.63 crores adjustment related to upstream exploration and production technical services rendered under Production Sharing Contract frameworks, representing complete substantive victory for the assessee on this critical segment. This deletion was based on multiple converging legal and factual considerations.

Figure 4: Comprehensive analysis of multiple converging factors—including PSC framework supremacy, industry practice evidence, expert opinions, and revenue consistency doctrine—that led to complete deletion of the ₹48.63 crore adjustment

Analytical Framework Supporting Complete Deletion

Production Sharing Contract Framework Supremacy: Production Sharing Contracts (PSCs) are governed by formal agreements with the Government of India and receive specific parliamentary approval under Section 42 of the Income Tax Act, 1961. These contracts explicitly mandate at-cost remuneration among consortium members for technical services with absolutely no profit element permitted. This represents a legislatively recognized and sanctioned commercial framework that cannot be arbitrarily overridden through generic transfer pricing benchmarking exercises.

Industry Practice as Comparable Uncontrolled Price: Documentary evidence conclusively established that Shell group entities and joint venture consortium partners uniformly provide upstream exploration and production technical services strictly at cost under identical Production Sharing Contract frameworks across multiple jurisdictions and oil field projects. This uniform industry practice constitutes practical application of the Comparable Uncontrolled Price (CUP) method or permissible “other method” under Rule 10AB of the Income Tax Rules, fundamentally distinct from routine commercial IT-enabled services transactions.

Independent Expert Analysis and Documentary Support: The assessee provided comprehensive independent expert opinions from qualified petroleum industry professionals concluding that the at-cost recovery model represents the arm’s length standard for consortium technical services under Production Sharing Contract frameworks. This analysis was supported by actual intercompany service agreements, sample Production Sharing Contracts from multiple jurisdictions, and statutory auditor confirmations. The revenue authorities provided no meaningful counteranalysis or alternative benchmarking methodology.

Fundamental Methodological Violation: The Transfer Pricing Officer’s mechanical application of generic IT-enabled services comparables—including routine business process outsourcing providers, call center operations, and knowledge process outsourcing firms—to highly specialized upstream geological, geophysical, and reservoir engineering services performed under mandatory Production Sharing Contract frameworks was economically incoherent and fundamentally distorted the arm’s length principle.

Revenue Consistency Doctrine: The revenue authorities themselves had accepted the at-cost model in earlier assessment years for identical transactions and had similarly accepted the model for other consortium entities under the same Production Sharing Contracts. Selective departure in isolation without any change in underlying facts or applicable law is procedurally unjustified and violates principles of horizontal equity.

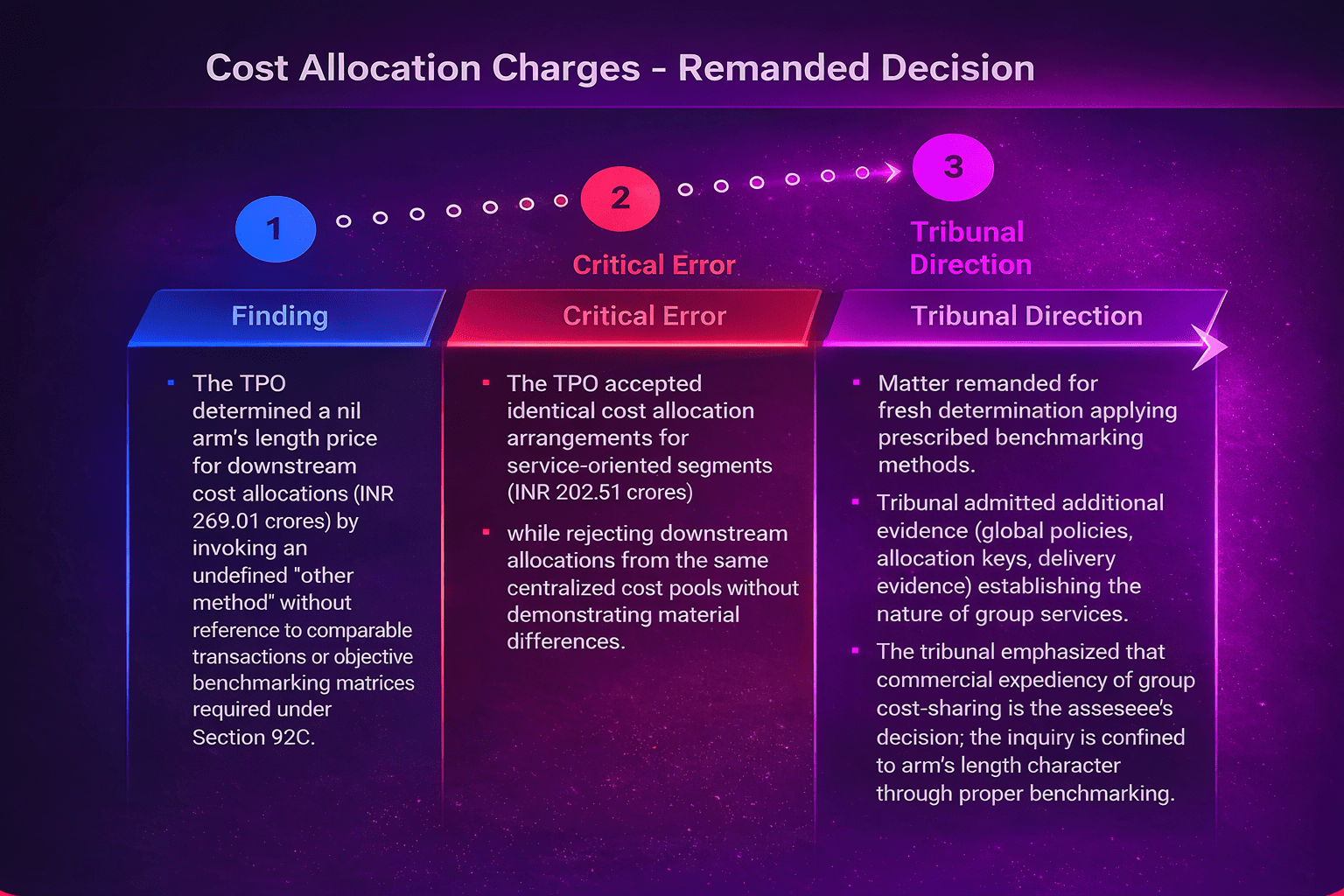

Issue IV: Group Cost Allocation Charges – Remanded with Critical Directions

Figure 5: Three-stage analytical framework applied by the tribunal in remanding the INR 269.01 crore cost allocation adjustment for fresh determination using proper transfer pricing methodologies with transparent benchmarking

The tribunal found that the Transfer Pricing Officer determined a nil arm’s length price for downstream cost allocations totaling INR 269.01 crores by invoking an undefined and unexplained “other method” without any reference to comparable market transactions or application of objective benchmarking matrices required under Section 92C of the Income Tax Act.

The critical analytical failure identified by the tribunal was the Transfer Pricing Officer’s inconsistent treatment: accepting identical cost allocation arrangements for certain service-oriented business segments (totaling INR 202.51 crores) while simultaneously rejecting functionally similar downstream cost allocations sourced from the same centralized group cost pools, all without demonstrating material differences in nature, scope, or economic substance.

Commercial Expediency Doctrine

The tribunal emphasized that commercial expediency considerations underlying intra-group cost-sharing arrangements represent the assessee’s legitimate business decision and organizational choice. The transfer pricing inquiry must be properly confined to verifying the arm’s length character of such arrangements through appropriate prescribed benchmarking methodology, not second-guessing the underlying business rationale or imposing alternative operational structures preferred by tax authorities.

The matter was remanded for fresh determination applying prescribed transfer pricing methods with proper benchmarking. The tribunal admitted additional evidence including global cost-sharing policies, detailed allocation key methodologies, and delivery confirmation evidence establishing the substantive nature of group services provided.

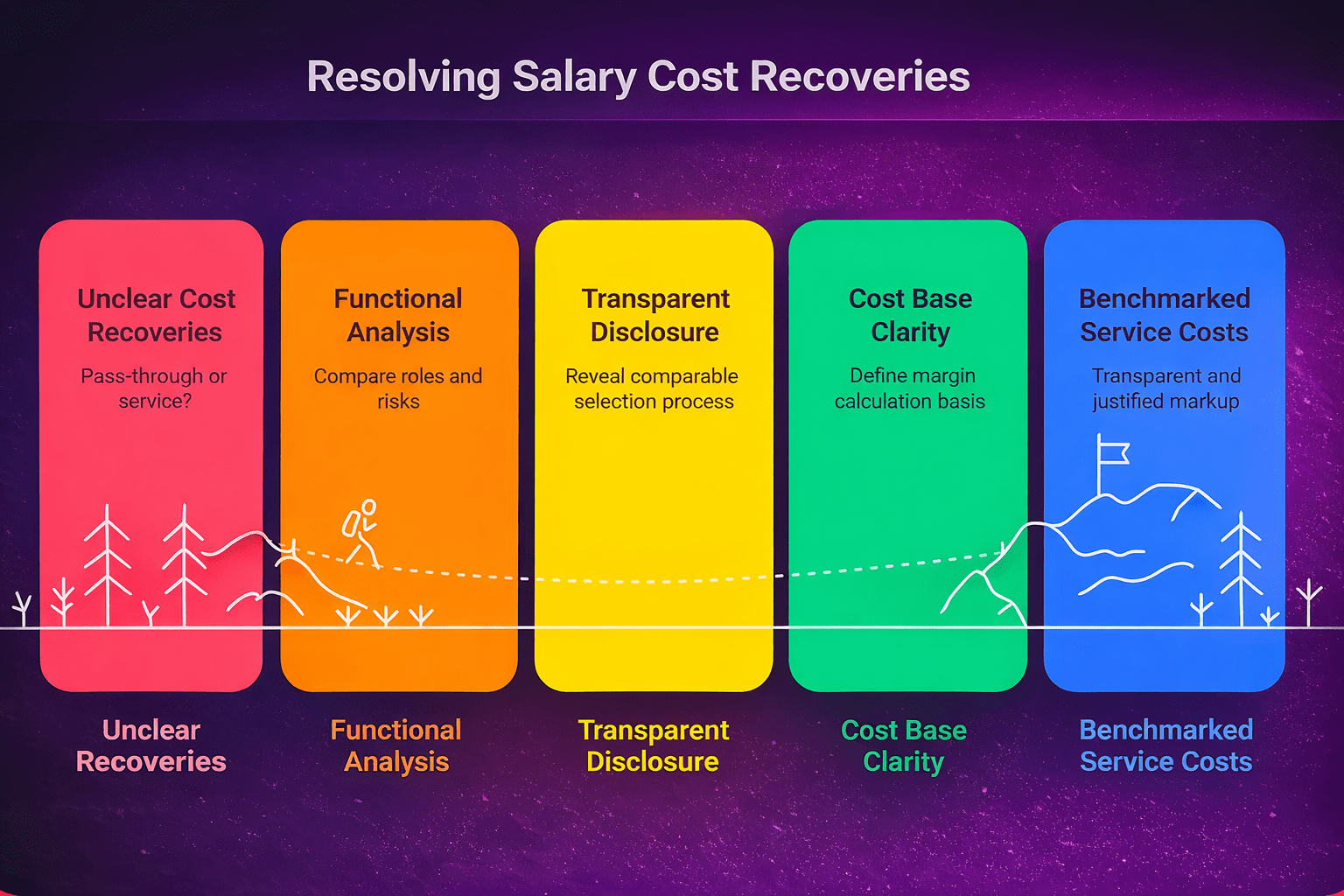

Issue V: Salary Cost Recoveries – Remanded for Proper Classification Analysis

Figure 6: Sequential five-step analytical process for determining whether secondment cost recoveries constitute genuine pass-through reimbursements or service transactions requiring arm’s length profit markup

The fundamental legal question presented was whether employee secondment cost recoveries charged on a pure cost-to-cost basis without any markup constitute genuine pass-through reimbursement items or instead represent independent service transactions requiring application of an arm’s length profit margin.

The tribunal found that the Transfer Pricing Officer mechanically recharacterized pass-through cost recoveries as “support services” and applied a Transactional Net Margin Method profit margin of 9.88% without conducting or transparently disclosing several critical analytical steps necessary to justify such recharacterization, including detailed functional analysis, transparent comparable selection process, clear cost base identification, and evidence of value-added activities or risk assumption.

The matter was restored for fresh adjudication to make two sequential determinations: first, whether the cost recoveries represent genuine pass-through items based on detailed functional analysis; and second, if services are ultimately found to exist, proper benchmarking using transparent comparable selection methodology with full disclosure of the margin computation basis.

Corporate Tax Matters: Additional Disallowances Resolved

Beyond the transfer pricing adjustments, the tribunal addressed several corporate tax disallowances, providing relief to the assessee on multiple fronts:

Section 40(a)(ia) Disallowance (INR 8.82 lakhs) – ALLOWED

The Dispute Resolution Panel had already directed deletion of this disallowance after verification of TRACES records demonstrating that apparent technical errors had been corrected. The Assessing Officer is statutorily bound to follow Dispute Resolution Panel directions under Section 144C. The tribunal held that continuance of the disallowance was legally unsustainable and directed immediate deletion.

Duplicate Disallowance (INR 22.50 lakhs) – ALLOWED

The assessee had already voluntarily disallowed merger-related expenses in the filed return of income. The Centralized Processing Centre made a duplicate disallowance due to a mismatch in the Tax Audit Report presentation. The tribunal issued directions to verify underlying records and ensure no double disallowance occurs.

Advance Tax Credit (INR 5.33 lakhs) – ALLOWED

Advance tax paid by the amalgamated entity (Pennzoil Quaker State India Limited) was properly reflected in Form 26AS. The assessee became entitled to this credit post-amalgamation under applicable merger accounting principles. The tribunal directed verification of payment challans and Form 26AS with grant of appropriate credit.

Critical Compliance Implications for Multinational Enterprises

Strategic Takeaways for Transfer Pricing Risk Management

This ITAT Mumbai ruling establishes core compliance standards and procedural requirements that will fundamentally shape transfer pricing enforcement, audit defense strategies, and documentation best practices for multinational enterprise groups operating in India. The decision elevates previously discretionary best practices into mandatory compliance requirements with direct impact on audit outcomes and litigation success rates.

Multinational enterprises should undertake immediate comprehensive internal reviews of existing transfer pricing documentation, comparable company selection methodologies, and industry-specific framework recognition to ensure full alignment with the standards established in this landmark ruling.

Priority Action Items for Immediate Implementation:

- Contemporaneous Data Audit: Conduct thorough review of all transfer pricing studies to verify that comparable company selections utilize exclusively current-year financial data for the relevant assessment year, not mechanically recycled datasets from prior assessment periods

- Filter Methodology Validation: Document clear, specific economic rationale for any quantitative filters (revenue thresholds, asset size criteria, employee count ranges) applied during comparable company screening process, ensuring filters serve legitimate data quality objectives rather than result-oriented exclusion purposes

- Specialized Framework Integration: For group entities operating under specialized regulatory or contractual frameworks (Production Sharing Contracts, regulated utility rate structures, government concession agreements, consortium arrangements), ensure transfer pricing analysis properly incorporates and reflects these commercial and legal constraints with supporting documentation

- Cost Allocation Documentation Enhancement: Develop and maintain comprehensive documentation of all intra-group cost allocation methodologies, including detailed allocation key formulas, actual service delivery evidence, quantified benefit analysis, and benchmarking support demonstrating arm’s length character of allocation charges

- Reimbursement vs. Services Classification Analysis: Implement clear internal protocols and decision trees for distinguishing genuine cost reimbursements from independent service transactions, incorporating assessment of functional value-addition, risk assumption patterns, and service recipient benefits

Conclusion: Five Pillars of Controlling Legal Authority

Final Case Outcome Summary

Total Transfer Pricing Adjustments Largely Set Aside

₹48.63 Crores (Exploration & Production segment) entirely deleted with immediate effect | ₹481.52 Crores remanded to lower authorities for fresh determination following binding tribunal directions | Multiple corporate tax disallowances overturned

The Income Tax Appellate Tribunal Mumbai’s comprehensive decision in Shell India Markets Private Limited establishes binding controlling precedent across five critical dimensions of transfer pricing law, procedure, and substantive analysis:

- Contemporaneous Data Statutory Mandate: Rule 10B(5) requires current-year comparable company searches as the foundational element of legally compliant and analytically reliable transfer pricing determinations. Mechanical importation of prior-year comparable selections across multiple assessment years without fresh analysis violates express statutory requirements and produces systematically unreliable arm’s length pricing conclusions.

- Arbitrary Filter Prohibition Doctrine: Turnover-based or size-based quantitative filters applied after completion of detailed functional, asset, and risk comparability analysis for the purpose of excluding otherwise functionally comparable entities constitute impermissible result-oriented “cherry-picking.” Such post-hoc mechanical exclusions lack economic logic and fundamentally distort arm’s length price determinations.

- Production Sharing Contract At-Cost Model Legal Recognition: Industry-uniform at-cost service provision practices among consortium members operating under government-approved Production Sharing Contracts with parliamentary sanction represent valid industry norm equivalent to Comparable Uncontrolled Price methodology. Such specialized legal and regulatory frameworks cannot be overridden through mechanical application of generic information technology services benchmarking that ignores fundamental economic, legal, and risk allocation differences.

- Intra-Group Services Commercial Expediency Recognition: Commercial expediency and operational efficiency considerations underlying intra-group service arrangements and cost-sharing mechanisms represent legitimate business decisions properly within the taxpayer’s autonomous business judgment domain. Transfer pricing regulatory analysis is properly limited to verifying arm’s length character through appropriate prescribed benchmarking methodologies, not second-guessing strategic business decisions or imposing alternative organizational structures preferred by revenue authorities.

- Dispute Resolution Panel Binding Directions Doctrine: Assessing Officers possess no legal authority to ignore, dilute, or selectively implement directions issued by the Dispute Resolution Panel under Section 144C of the Income Tax Act. Such directions constitute binding components of the continuing assessment process, and willful non-compliance renders subsequent assessment actions legally unsustainable and void.

This comprehensive decision provides substantial immediate relief to Shell India Markets Private Limited while simultaneously establishing critical procedural guardrails and substantive analytical frameworks that will fundamentally shape transfer pricing methodology development, documentation quality standards, audit defense strategies, and dispute resolution processes for multinational enterprise groups operating across all industry sectors in India.

Ensure Your Transfer Pricing Framework Meets Tribunal Standards

The Shell India Markets ruling demonstrates that technical precision in transfer pricing documentation, comparable selection methodology, and industry framework recognition is no longer discretionary—it represents essential foundational requirements for successfully defending against aggressive revenue positions and audit challenges.

Strategix International specializes in developing tribunal-ready transfer pricing frameworks:

Transfer Pricing Documentation & Compliance Strategy | Advanced Functional Comparability Analysis | Industry-Specific Framework Development & Integration | Dispute Resolution & Appellate Litigation Support | Proactive Regulatory Risk Assessment & Management

Explore Transfer Pricing Advisory Services