OECD Guidance on Common Errors in Country-by-Country Reporting.

What multinational groups are getting wrong, and why it matters for global transfer pricing risk.

Country-by-Country (CbC) reports are a primary input for transfer pricing risk assessment and BEPS enforcement worldwide. The OECD has issued critical guidance after identifying recurring, systemic errors in filed reports.

Accurate and consistent CbC data is critical; errors directly undermine the reliability of risk analysis and the effectiveness of bilateral treaty exchanges between tax authorities. This briefing outlines the critical error taxonomy identified by the OECD.

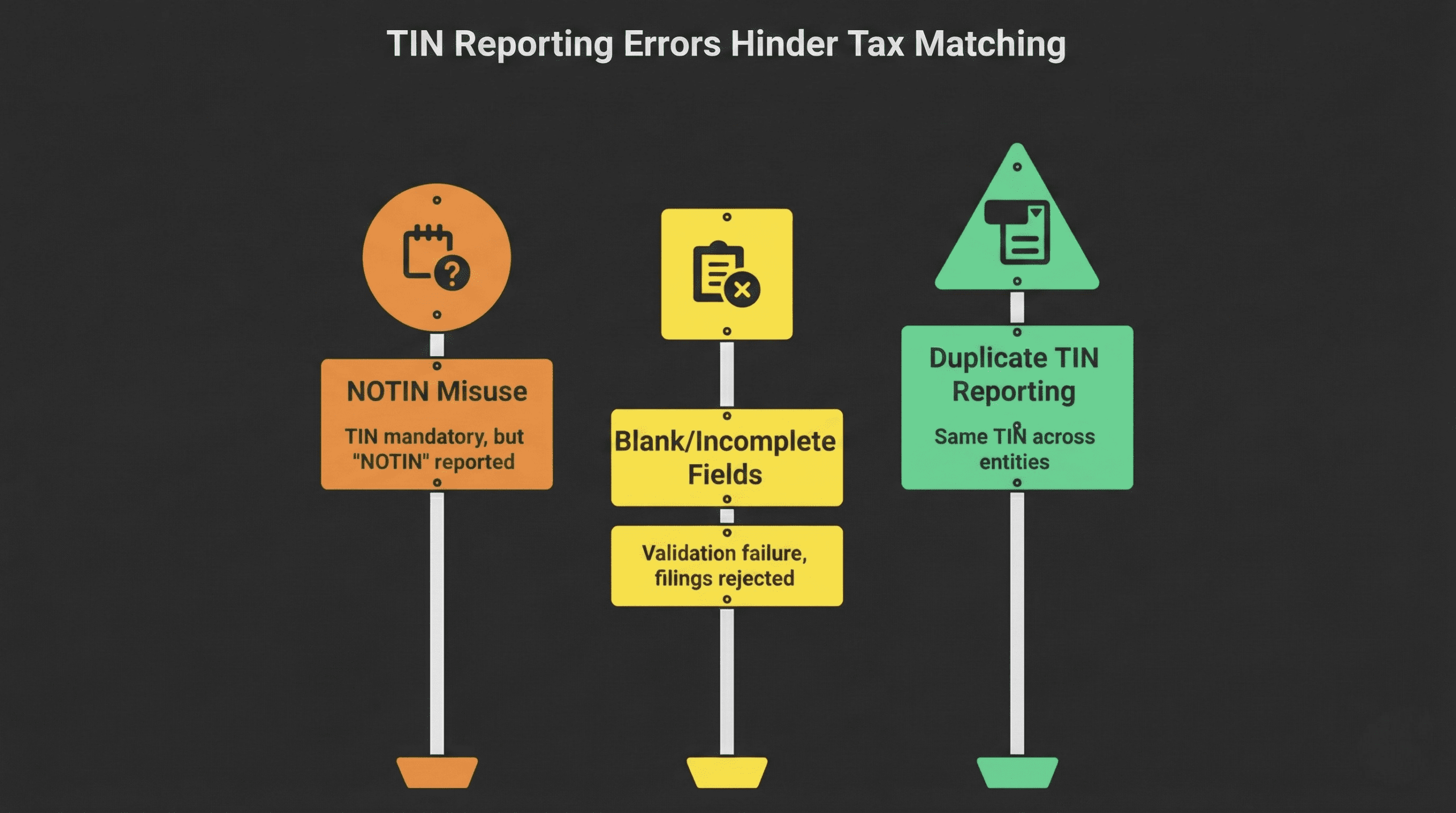

Tax Identification Number (TIN) Errors: The Gatekeeping Problem

TIN errors are among the most serious Country-by-Country reporting errors because they prevent tax authorities from reliably identifying and matching constituent entities. The OECD highlights three recurring, high-risk issues:

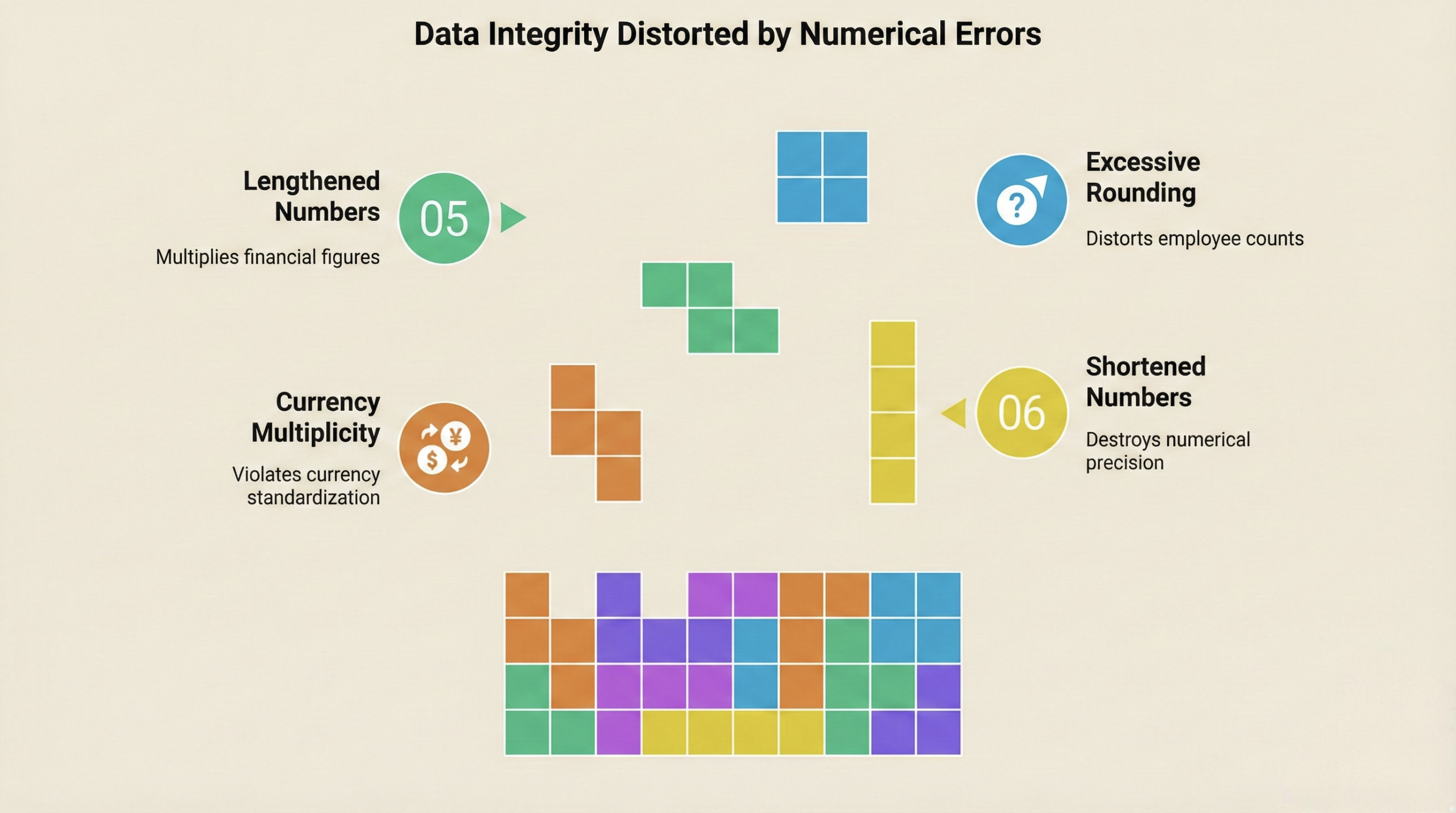

Numerical and Currency Formatting: The Data Integrity Layer

Errors in numerical and currency reporting directly compromise the reliability of CbC data used for risk assessment. The OECD identifies four high-impact issues:

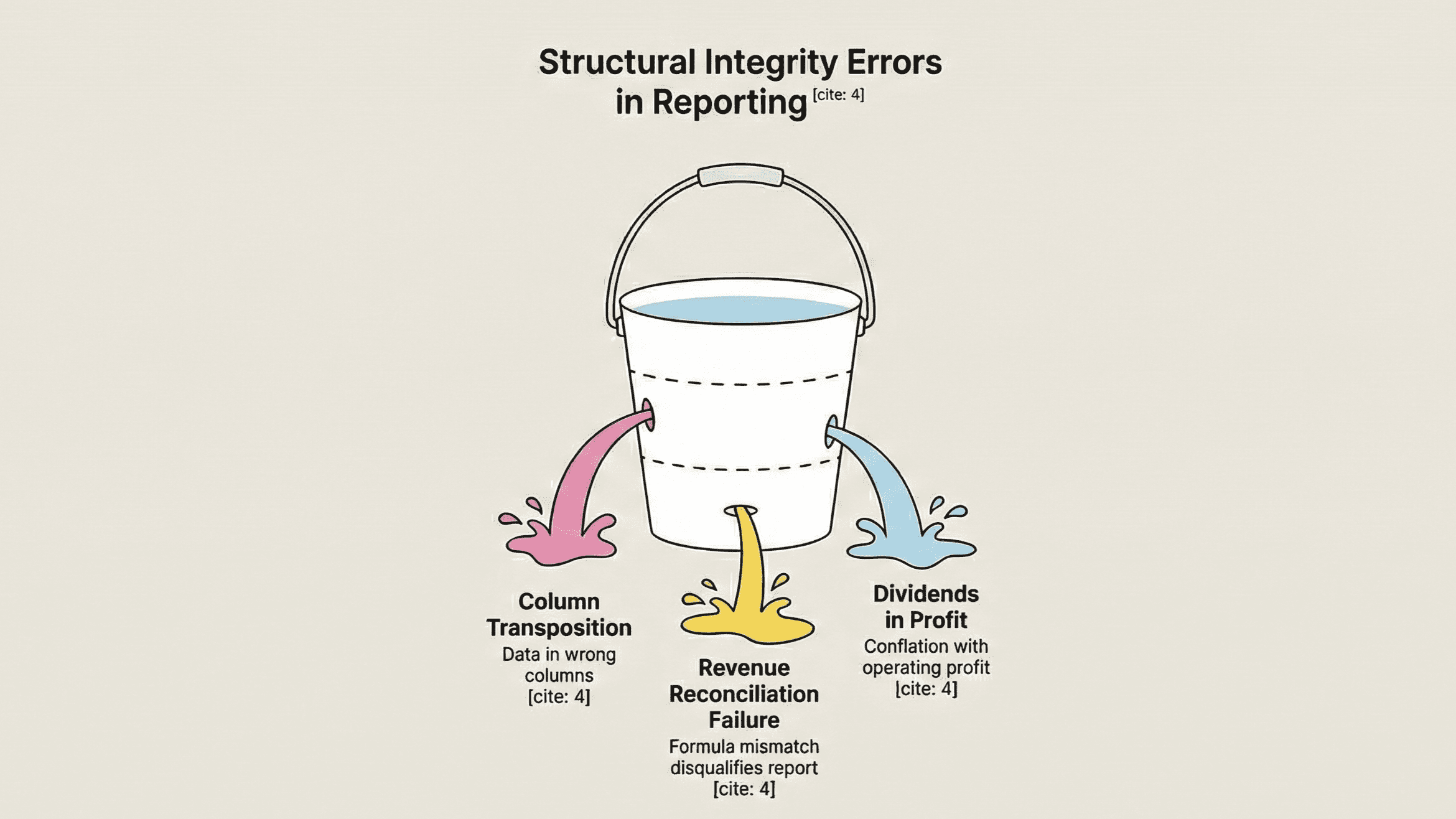

Table 1 Structural Integrity: The Logic Validation Layer

Structural errors in Table 1 indicate fundamental weaknesses in data validation and reconciliation. The OECD highlights two critical failures:

Column Transposition: Financial and non-financial data is reported in incorrect columns, producing internally inconsistent results that are mathematically implausible.

Revenue Reconciliation Failure: Total revenues must equal the sum of related and unrelated party revenues. Omissions, particularly extraordinary income or investment gains, create reconciliation breaks that invalidate the report.

Furthermore, dividends from constituent entities are frequently incorrectly included in profit (loss) before tax. OECD guidance explicitly prohibits this treatment, requiring clear separation from operating results.

Entity Scope Completeness: The Definition Problem

Misinterpretation of “Constituent Entity” leads to incomplete and non-compliant CbC filings that misrepresent the group’s global footprint.

Business Activity & Versioning

The Characterization Problem

Errors in business activity classification weaken the analytical value of Table 2 and raise immediate red flags. This includes incorrect activity classification (e.g., mislabeling marketing as manufacturing) and improper use of “Other” without clear explanation in Table 3.

The Timeline Problem

Failure to split extended periods: The Reporting Period must reflect the group’s fiscal year-end, not the filing date. When a fiscal year exceeds 12 months, separate CbC reports are mandatory for each financial statement period.

Exchange Rate and Source Data Disclosure

Where statutory financial statements are used as the data source, all amounts must be translated into the Ultimate Parent Entity’s functional currency using the average exchange rate for the reporting period. This rate must be disclosed in Table 3. Failure to disclose the exchange rate prevents tax administrations from validating the accuracy of the reported CbC information.

Practical Compliance Implications

CbC is no longer peripheral; it must be treated as a core compliance and risk-management tool. TIN inaccuracies and incomplete entity coverage increasingly act as early risk flags for tax authorities.

Ensure your reporting framework is inspection-ready.